It was a fun little conversation about mediocre pitchers and the massive contracts they nevertheless command, but it brought to mind what has come to be known as one of the worst contract negotiations in history--the Bobby Bonilla buyout by the Mets.

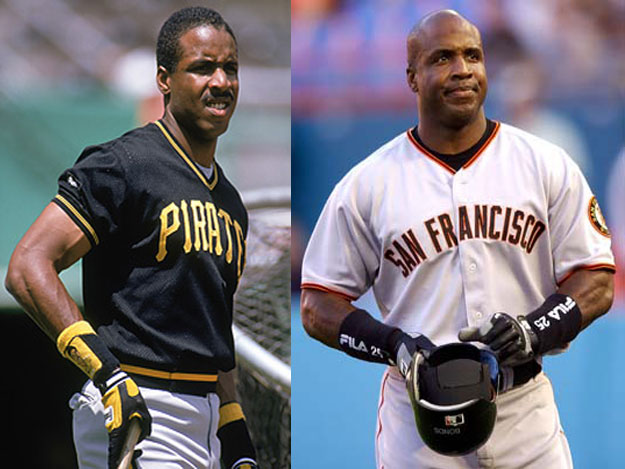

For those who are unfamiliar, Bobby Bonilla was once a very talented outfielder. As a Pittsburgh Pirate, Bonilla teamed with Andy Van Slyke and pre-steroid Barry Bonds to form one of the game's best outfields, leading the Pirates to consecutive division titles in 1990 and 1991 (yeah, it was a long time ago). Bonilla was a big part of the team's success--he was an All-Star every year from 1988 to 1991, and he finished in the top 3 of MVP voting in both 1990 and 1991 (2nd in 1990 behind Bonds, 3rd in 1991 behind Bonds and Terry Pendleton).

{kind=link}

After his second MVP-caliber season, the Mets rewarded him with an enormous (by 1991 standards) free agent contract, luring him away from the Pirates with a 5-year, $29 million deal. It didn't work out. His performance was adequate (though not meeting his previous level), and he even earned two All-Star nods during the first four years of the contract. But Bonilla wilted under the New York lights, clashing constantly with reporters and ultimately "earning" a trade to Baltimore in 1995.

That could have (and should have) been the end of it, but of course that's not the Mets way. After his original Mets contract expired in 1996, Bonilla signed a four-year, $23.3 million contract with the Florida Marlins, and he immediately helped lead them to the 1997 World Series title. When the Marlins dismantled their roster in 1998, Bonilla landed in Los Angeles, and for reasons still unknown (maybe trying to atone for past sins), the Mets decided to re-acquire Bonilla via trade in 1999. Again, shockingly, it didn't work out.

With his relationship with his teammates, manager, and the media rapidly deteriorating, Bonilla and the Mets mutually agreed to a buyout of the final year of his Marlins contract, worth $5.9 million. Therein lies the problem.

The Mets at the time were a bit cash-poor (some things never change), and they decided that they didn't have the cash to both pay Bonilla and sign free agents to build their team for 2000. So they deferred Bonilla's compensation, arranging to not have to pay Bonilla a dime until 2011. Initially, this arrangement worked out--the Bonilla-free Mets made it to the World Series in 2000, and Bonilla would retire after two mediocre seasons in Atlanta and St. Louis.

But there's a bit of a problem here--interest rates. When the Mets deferred Bonilla's $5.9 million contract, the parties agreed to an interest rate of 8% (go ahead, try getting that rate today--no, not from Greece, that's cheating), with annual payments of $1.19 million a year for 25 years, beginning in 2011 (yes, the math works out--compounding is a powerful tool, which is why Bonilla will collect nearly $30 million in present-day money instead of $5.9 million in 1999 money).

Clearly, Bonilla got the better end of this deal, essentially lending money at a fixed 8% rate in a steadily declining interest rate environment. Had Bonilla instead taken the $5.9 million at the time and invested it in the stock market... yeah, he wouldn't be happy.

To be fair to the Mets, at the time, 8% was a completely fair interest rate at which to effectively "borrow" money from Bonilla. In January of 2000, a 30-year fixed rate mortgage would have run about 8.3%, and the average rate throughout the year 2000 was about 8.05%. Furthermore, recent history suggested that long-term rates were more likely to go higher rather than lower--rates had exceeded 10% throughout the entire decade of the 1980s, and they were nearing multi-decade lows (thanks, Alan Greenspan).

Whether or not the Mets were making a bet on rising interest rates (it's possible, but we'll never know), they certainly wouldn't have been alone in their analysis. Institutions like the Port Authority of New York/New Jersey have lost millions of dollars after entering into swaps that would protect them from rising rates, and it would have been difficult for anyone--let alone a baseball franchise--to predict the low-interest rate environment that we've experienced over the past decade.

But that won't keep people from laughing at the Mets, and wondering whether Bobby Bonilla (or his agent) was the greatest interest rate trader of all time. Either way, because of their poor interest rate bet, the Mets this year began paying Bonilla more than several of their current (contributing) players currently earn.

Bonilla, for his part, seems humble--as he told the Wall Street Journal, "hey, a blind squirrel can find an acorn". Indeed. Especially when that blind squirrel plays for the Mets.

No comments:

Post a Comment